Medical Education

May 2025

Peer-Reviewed

Private equity (PE) margin maximization and profit-making strategies focus on acquisition, short-term ownership, and sale of health care entities, including residency program opportunities. PE ownership durations generally have 3 purposes: reduce staff, sell assets, and refinance debt. The purpose of graduate medical education (GME), however, is to provide learning and training opportunities in a variety of clinical, academic, technical, and research domains. This article offers examples of PE involvement in residency training and argues that PE and GME purposes not only conflict but add instability to graduate medical education learning environments. This article also suggests reasons why PE investment in GME, including residency “slot” ownership, undermines academic health centers’ ethical and educational obligations to trainees in their GME programs.

For 135 years, postgraduate resident education has been a core component of a physician’s extensive training, during which a recent graduate grows into a practicing physician.1 All the while, this has been done under the close stewardship of academic health professions institutions, with education as their priority. The goals of residency include training future generations of physicians with a primary focus on clinical skills, ethics, academics, and research. Residents, through clinical exposure during training and mentorship from their teachers and colleagues, are expected to grow into independently practicing physicians. Residents are taught through patient-centered care that prioritizes patient outcomes and allows for learning opportunities. Moreover, residents are given protected time for education and scholarship.

Purchase by private equity (PE) and other profit-focused entities of residency “slots” directly conflicts with the above-stated goals. Exploiting residency slots as an investment detracts from the long-standing institution of residency training by undermining the stability of training programs. PE’s goal is simple: to acquire a business, cut costs and make it more valuable, and then sell the business within a relatively short period of around 5 to 10 years.2 PE firms also have tax advantages and lack certain regulatory oversight that publicly traded companies have.2 Residency programs owned by PE firms have the unnecessary burden of worrying about when, not if, their hospital and training program will be sold to another profit-focused entity.

Commodification of residency slots by PE frames these training slots as an asset that can be leveraged in financial transactions or used to generate profit rather than as a key component of medical education that represents an investment in the future of health care in the United States. Viewing residents as assets or employees rather than as trainees can have downstream effects, as residents are expected to boost profit by maximizing numbers of patients they see and numbers of procedures in which they participate rather than focusing on their education. Unsurprisingly, given residents’ financial and work stress, institutions are seeing a growing trend toward trainee unionization, with the goal of affording some protection of the priorities of trainees.3 Moreover, if PE firms own and operate hospitals in order to decrease costs and only care for patients with less complex and therefore less costly problems, trainees at those institutions will lose the exposure to and training in caring for more critically ill patients.4 This loss could influence their skill development and ability to care for such patients in the post-training environment. In other ways as well, PE firms’ cost-cutting orientation could create inequity between PE-owned and non-PE owned programs. Given the PE emphasis on decreasing costs, trainees at PE-owned institutions could have fewer resources for and less guidance in providing quality services. Each of these factors can affect the quality of a resident’s education and career development. They can also affect the quality of and access to care provided by trainees at PE-owned hospitals.

This paper examines the history of residency programs, their current structure and funding, the growth of PE in health care, and why PE firms should not own residency positions.

The basis of the current residency training structure in the United States was introduced 135 years ago.1 Accrediting bodies, specialization, and subspecialization took root in the first half of the 20th century.5 Residency slots grew exponentially following World War II, and, by 1975, residency programs were the ubiquitous standard for medical students following graduation from medical school.5 While residency training has undergone changes, the standard of creating a cohesive training environment that emphasizes learning by participating in patient care has remained the same.

The majority of resident training positions are funded by the federal government.6 This federal funding has been provided since 1965, following the establishment of the Centers for Medicare and Medicaid Services (CMS).7 In 2015, the federal government allocated approximately $15 billion to graduate medical education (GME), with Medicare providing the majority (71%) of this funding.8 Medicaid contributed 16%, while the Veterans Health Administration accounted for 10%.8 The remaining support comes from various other federal sources.8

Medicare imposes caps on direct and indirect payments to teaching hospitals.6 According to the US Government Accountability Office, 70% of teaching hospitals were over at least one cap and half of hospitals in counties with clinician shortages were over both caps in 2018.6 These health systems and hospitals utilized other funding sources, including state and private, to fund training positions beyond their cap.6 Direct payment is based on a hospital’s number of resident physicians and Medicare patient volume, while indirect payment is based on the ratio of resident physicians to inpatient beds.7 In 2018, roughly 70% of teaching hospitals and hospital systems funded more residency slots than their allotment from CMS, while only 20% of hospitals funded under their allotment.6 This trend could, in part, be due to the lack of growth of CMS-funded residency slots, which was capped in 1997 by Congress at 1996 levels.7 Congress granted federal funding for 1000 new residency slots in 2020, which was the first time CMS-funded residency slots were increased since 1997.7

This slow growth of government residency funding leads us to question how profit-oriented, short-horizon entities like PE firms would approach residency funding in an acquired hospital or hospital system. As mentioned, PE works by acquiring a business to grow the revenue of the company, reducing costs, refinancing debt, and then exiting through a sale.9 There is genuine concern that a PE-owned hospital could cut certain funding to residency slots, such as funding for educational enrichment and scholarly activity, in the name of cutting costs. PE-owned entities can also seek to capitalize on GME training funding sources by maximizing patient volumes to increase revenue. It should be questioned whether PE-owned entities should be able to take advantage of government-funded residency slots intended for educating future physicians by regarding residents as affordable labor to increase profits.

Before we examine our core question of whether PE firms should own residency slots, we must look at the broader growth of PE in health care. Total PE investment in health care has increased tremendously over the past quarter century. PE investment in health care totaled $5 billion in 2000, climbed to $100 billion in 2018, and reached $200 billion in 2021.10,11 These firms invest in multiple areas of health care, including hospitals, nursing homes, and clinics.9 The number of acquisitions of physician practices has risen sharply (600% between 2012 and 2021), with PE firms tending to focus on lucrative practices such as dermatology, gastroenterology, and ophthalmology.10,11

Commodification of residency slots frames them as an asset that can be leveraged in financial transactions or used to generate profit rather than as a key component of medical education.

PE’s ownership of hospitals has been even more substantial. PE firms now own around 30% of for-profit hospitals in the United States (460 hospitals).12 Patient care often suffers in hospitals owned by PE. A recent study in JAMA found that PE acquisitions were associated with a 25% increase in hospital-acquired adverse events, such as falls and certain infections, relative to control hospitals.13 Moreover, these hospitals tended to admit lower-risk and younger patients while increasing transfers of more complex patients to other hospitals.13

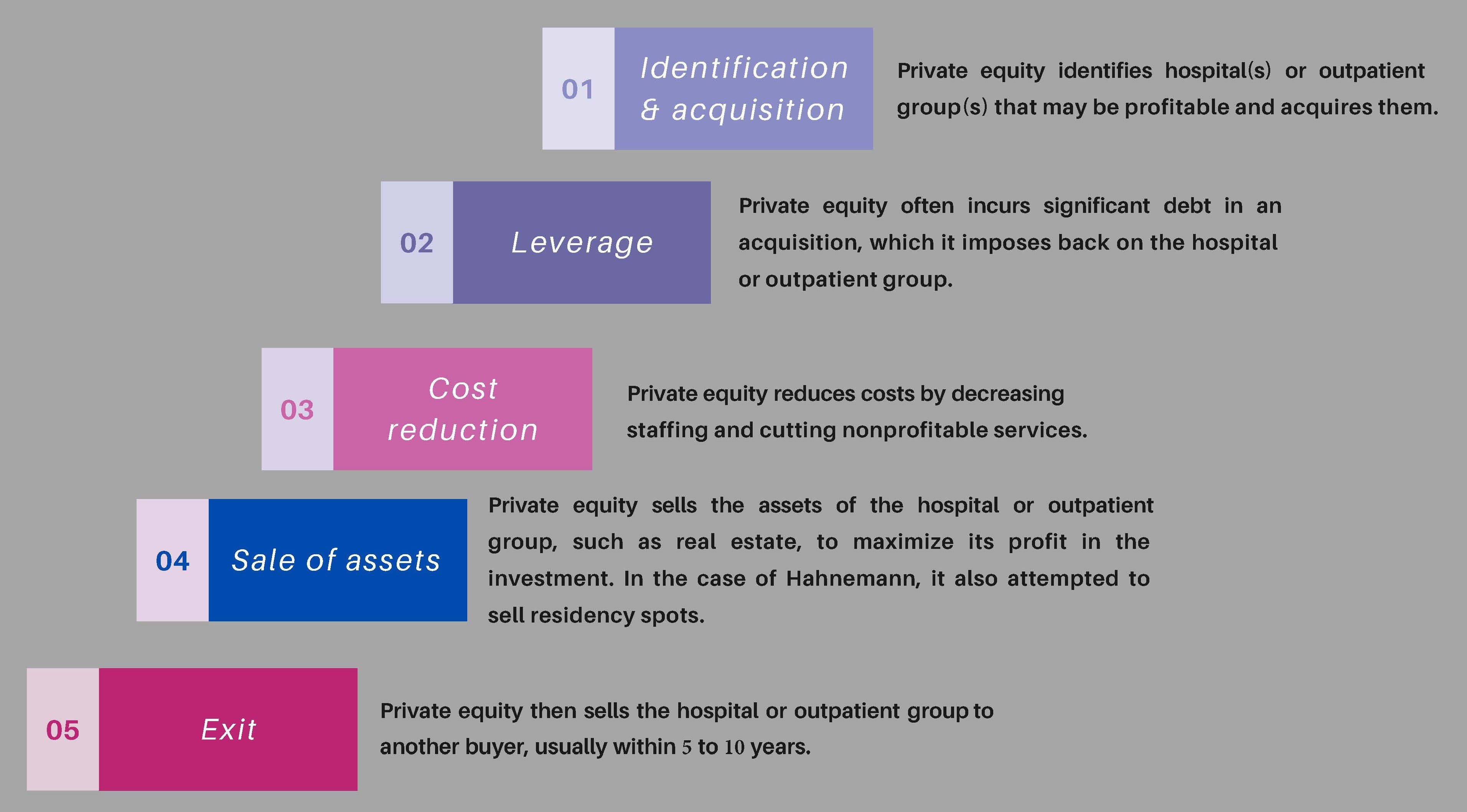

In order to purchase hospitals and outpatient groups, PE firms assume significant debt, which, in turn, is placed on the hospitals or outpatient groups2 (see Figure). Companies that are acquired via such a leveraged buyout have a 10-fold increased risk of going bankrupt.2 There have been several poignant examples of hospitals saddled with debt experiencing supply and staffing shortages, closures, and a systematic bleeding of assets.14,15 Staffing shortages can further burden residents in these hospitals and affect the quality of care provided.16 Additionally, hospital closures not only devastate their surrounding communities but also disrupt medical residency training, leaving physicians-in-training facing uncertainties about their educational future. This is exactly what happened at Hahnemann Hospital in Philadelphia, Pennsylvania, which mostly serves underserved patients whose care is covered by Medicare and Medicaid.

Figure. Private Equity Hospital and Outpatient Group Acquisition

Hahnemann Hospital had financial hardships for decades and was bought by a for-profit health care company, Tenet Heath, in 1998.17 The hospital, along with its 570 residency spots, was sold in 2018 to an affiliate of Paladin Healthcare Capital—a PE firm focused on smaller hospitals—in partnership with a real estate-focused PE firm.17 This acquisition led to suspicion that the hospital was purchased for redevelopment purposes rather than for sustaining a teaching hospital vital to its community. The hospital filed for bankruptcy and was closed in 2019, although the real estate was not included in the bankruptcy.17 At the same time, the PE company attempted to sell the 570 federally funded residency slots, circumventing regulations set by CMS.17 This sale was initially approved by a bankruptcy judge but was halted following an appeal by CMS.17

This case provides an example of the negative effects of PE on both the community and trainees. To our knowledge, it is the only example in the literature of a PE firm completely owning residency slots. However, as PE grows its market share in hospitals and outpatient groups, its interactions with residents are likely to grow. These interactions can range from PE firms directly owning and administrating residency slots, which is what happened at Hahnemann, to residents completing a short rotation (1-2 months) at PE-owned hospitals or clinics. The Hahnemann example highlights the ethical conflict between PE and residency training. Rather than seeing its residency slots as a responsibility to protect and ensure the continuation of trainees’ vital education, the PE firm attempted to financially leverage its residency slots in its bankruptcy case while ensuring that it retained the real estate of Hahnemann. Trainees should be assured of the stability of their residency program and be protected from events that can impact the progression of their training. The PE firm violated that trust.

Following the Hahnemann closure, the American Medical Association called for added protections for trainees, greater oversight of hospital closures, and policies for clinical site closures.18 The American Academy of Family Physicians echoed calls for close oversight and regulation of PE-funded residencies.19 Additionally, the president of the Accreditation Council for Graduate Medical Education (ACGME) and coauthors addressed the Hahnemann incident in a commentary in Academic Medicine.20 This commentary laid out the ACGME’s plan to deal with future closures. This plan includes soliciting resident input on how to support well-being in situations like Hahnemann and developing tools and protocols to address future interference in GME.20 The commentary stopped short of directly addressing PE.

The ACGME should, however, directly address PE. Among the ACGME’s vision elements are advancing graduate medical education in health care delivery systems that equitably meet local and regional community needs and developing residents and fellows who prioritize the needs of patients and their communities.21 The Hahnemann closure starkly illustrates the conflict between PE and the ACGME’s vision. The PE firm strategically closed a safety net hospital serving an underserved community—choosing profit over community health needs and thereby directly contravening the principle of equitable health care delivery.

To our knowledge, there is scant literature examining or discussing the impact of PE on managing teaching hospitals and their residents. Hahnemann was a large hospital with a considerable number of training positions, and these GME slots were up for sale less than 2 years after PE acquisition of the hospital. There are numerous large hospital systems and universities that operate under one GME umbrella. These systems have hundreds and sometimes thousands of residency slots. It is doubtful that PE leadership would be properly equipped or competent to handle a hospital system with a large share of Medicare-funded residencies. Unlike traditional hospital leadership with backgrounds in academic medicine, PE executives approach health care primarily from a financial perspective. This disconnect leaves them unprepared to navigate the complex requirements of residency programs, including accreditation standards, medical education delivery, and the balance between service and education—all essential components of running a teaching hospital system.

There are a few examples of trainees working in PE-owned clinical practices, particularly in dermatology. A large share of the clinical sites for the dermatology residency at the Kansas City University of Medicine and Biosciences Graduate Medical Education Consortium are PE-owned dermatology practices. The company that owns these clinical sites provided residents with a stipend of $10 000 and the option of a yearly $30 000 loan, which was paid back following completion of training or was forgiven if trainees signed a contract with the PE-backed dermatology practice,22 but this program has since ended. PE can provide financial incentives to academic institutions as well. In 2019, Rush University Medical Center agreed to a clinical and academic affiliation with a PE-backed large dermatology group for an ownership share in the group.23

Both of these examples show how PE provides financial incentives to academic institutions and residents to be involved in PE-backed residency training. If trainees work in PE-owned hospitals and outpatient groups, it is imperative that residency training be solely managed by academic institutions with close, quality oversight. Government should regulate the financial relationship that academic institutions can have with PE, as well as strictly oversee what a PE firm can provide trainees in the form of salary and incentives.

The negative impact of PE on health care and GME is clear. PE firms have shown a willingness to use residency slots as commodities to sell for profit without regard for residents’ training progression and the communities these residents serve. They have financially incentivized residents to rotate in their practices as a means for recruiting. PE ownership threatens resident training through multiple mechanisms: chronic staffing shortages that compromise supervision, reduced exposure to complex patients, diminished educational and scholarly opportunities due to budget cuts, and a focus on revenue generation that undermines the educational mission.

There is a need for added regulation and legislation to monitor PE’s encroachment in health care, including residency training. The goals of residency training and PE do not align. Residency training should be in a stable environment where the focus is on learning, professional growth, and providing patient-centered care. PE does not provide this stability, given its short timeline for exits and propensity to close or indebt hospitals. PE provides an environment focused not on learning but rather on increasing revenue and cutting costs. PE-owned hospitals also can struggle to teach trainees patient-centered care given their higher incidence of adverse events,13 overextended staff, and focus on more lucrative specialties.10,11

PE has, in large part, been shown to have had a negative impact on health care. The case of Hahnemann Hospital made clear that the PE firm was disingenuous in its commitment to the community, physicians, and trainees. Residencies were seen as commodities, and they were nearly auctioned in bankruptcy court. Residency slots should never be seen as an asset that generates revenue but rather as an obligation to train the medical workforce of the future. If the goal of the training program is to provide dollars to the bottom line, then physician training will be shortchanged.

The history of residency—and what lies ahead. American Medical Association. November 19, 2014. Accessed November 11, 2024. https://www.ama-assn.org/education/improve-gme/history-residency-and-what-lies-ahead

Tkacik M. Private equity gloats over a doctor glut. The Lever. May 20, 2022. Accessed December 7, 2024. https://www.levernews.com/private-equity-gloats-over-a-doctor-glut/

Rosenberg M. Physician workforce: caps on Medicare-funded graduate medical education at teaching hospitals. US Government Accountability Office; 2021. GAO-21-391. Accessed April 8, 2024. https://www.gao.gov/assets/gao-21-391.pdf

Physician workforce: HHS needs better information to comprehensively evaluate graduate medical education funding. US Government Accountability Office. March 9, 2018. GAO-18-240. Accessed April 8, 2024. https://www.gao.gov/products/gao-18-240

Morran C, Petty D. What private equity firms are and how they operate. ProPublica. August 3, 2022. Accessed April 8, 2024. https://www.propublica.org/article/what-is-private-equity

Blumenthal D. Private equity’s role in health care. The Commonwealth Fund. November 17, 2023. Accessed April 9, 2024. https://www.commonwealthfund.org/publications/explainer/2023/nov/private-equity-role-health-care

PESP Private Equity Hospital Tracker. Private Equity Stakeholder Project. Accessed March 25, 2025. https://pestakeholder.org/private-equity-hospital-tracker/

Garber J, Daniels I. Steward implosion provides cautionary tale on private equity in health care. Lown Institute. March 19, 2024. Accessed April 8, 2024. https://lowninstitute.org/steward-implosion-provides-cautionary-tale-on-private-equity-in-health-care/

Elkind P, Burke D. Investors extracted $400 million from a hospital chain that sometimes couldn’t pay for medical supplies or gas for ambulances. ProPublica. September 30, 2020. Accessed April 8, 2024. https://www.propublica.org/article/investors-extracted-400-million-from-a-hospital-chain-that-sometimes-couldnt-pay-for-medical-supplies-or-gas-for-ambulances

Landman K. The profit-obsessed monster destroying American emergency rooms. Vox. October 3, 2024. Accessed December 7, 2024. https://www.vox.com/health-care/374820/emergency-rooms-private-equity-hospitals-profits-no-surprises

Murphy B. Address private equity’s growing impact on residency training. American Medical Association. November 16, 2022. Accessed April 10, 2024. https://www.ama-assn.org/education/gme-funding/address-private-equity-s-growing-impact-residency-training

Graduate medical education financing policy. American Academy of Family Physicians. October 2023. Accessed January 27, 2025. https://www.aafp.org/about/policies/all/graduate-medical-education-financing.html

Mission, vision, and values. Accreditation Council for Graduate Medical Education. Accessed October 25, 2024. https://www.acgme.org/about/overview/mission-vision-and-values

Konda S, Francis J, Motaparthi K, Grant-Kels JM; Group for Research of Corporatization and Private Equity in Dermatology. Future considerations for clinical dermatology in the setting of 21st century American policy reform: corporatization and the rise of private equity in dermatology. J Am Acad Dermatol. 2019;81(1):287-296.e8.